Confidentiality Matters Pt I - Fight for the Future Report

Overview of a recent report on financial privacy

When you’re posting about your favorite bands (and their political views) on social media, or donating to support mutual aid or harm reduction organizations, most people aren’t thinking about digital footprints or data surveillance. But the unfortunate reality is that today—where even simple transactions leave behind a data trail—“privacy” has taken on a whole new urgency. Mutual aid groups, from abortion funds to bail funds and even those simply distributing food, are finding themselves in the crosshairs.

In this two part series we’ll look at why confidentiality is so important, especially today. Part I will look at a recent report on financial privacy and in Part II we speak with someone helping build usable private financial products.

The report “Financial Confidentiality in the Age of Digital Surveillance” (produced by Fight for the Future and Convocation Research+Design) underscores why communities urgently need modern financial tools that keep data secure.

Below is a broad-strokes look at the report’s key findings, why these issues matter for mutual aid in and beyond the tri-state area, and how various technologies can help (or sometimes hinder) those who require privacy to stay safe and protected. Please do read the full report which goes into great detail on all of these topics and subscribe so you don’t miss Part II.

Why Financial Privacy Matters

For the countless grassroots projects, financial privacy is more than a luxury. In some places, receiving money for essential health services or donating to a community bail fund can lead to unwelcome scrutiny, shutdowns, or worse. Beyond the personal risk, a lack of privacy can chill the entire culture of mutual aid, stifling the momentum that’s driven so many scene-based relief efforts.

Without the ability to transact securely, groups that provide critical support—whether abortion funds, harm reduction programs, or other mutual aid networks—become vulnerable to financial censorship, legal targeting, and digital surveillance. This not only puts individuals at risk but also threatens the broader ecosystems of care that rely on trust, discretion, and freedom from outside interference. Financial privacy isn't just about anonymity; it's about ensuring that communities can sustain themselves without fear of retribution.

Where the Threats Lie

The report points to a variety of digital tracking tools—both within government agencies and private companies—that jeopardize anonymity. It discusses how data from financial apps can be subpoenaed or purchased, all while numerous digital platforms collect and store our payment histories. For communities working to support individuals in precarious situations—think abortion funds facing legal pressure in certain states—this level of surveillance can mean potential legal risk, social stigma, or worse.

Below are specific examples illustrating how digital tracking tools can jeopardize anonymity and create legal or social risks—particularly those supporting individuals in precarious situations such as abortion funds:

Subpoenas and Legal Requests to Exchanges

Many cryptocurrency and digital payment platforms must comply with Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations. The report notes that law enforcement agencies can issue subpoenas to these platforms, forcing them to hand over personal information tied to transactions. Once a subpoena links a person’s identity to a payment address, the rest of their transactions (past and future) can become visible to investigators.

IP Address Collection

Several platforms discussed in the report (such as Privacy.com or mobile wallet providers) collect users’ IP addresses, device identifiers, or location data. If compelled by law enforcement, the companies can disclose that network information. Even when the transaction amounts or account names are hidden, IP logs can be used to correlate users to specific devices, times, and places—effectively piercing pseudonymity.

Cooperation With “Blockchain Analysis” Firms

For cryptocurrencies like Bitcoin or partially private ones like Zcash (if used in “transparent” mode), the report points out that law enforcement often partners with specialized analytics firms (e.g., Chainalysis or CipherTrace). These firms have tools to trace transactions across the public ledger, clustering wallet addresses that likely belong to a single user or group. If one address is tied to an actual identity (e.g., via an exchange), the entire chain of related transactions may be revealed.

Data Retention by Payment Apps

Services such as Apple Cash, CashApp, PayPal, or any platform where real-world identity must be verified hold onto transaction histories and personal details. While the apps may not publicly share this data, it is stored on their servers and can be given to law enforcement upon request. The report warns that mutual aid groups deemed “risky” or “illicit” by these services can be suspended outright, cutting off an essential financial lifeline.

Purchasable Data From Third Parties

The report also highlights the gray market for personal data—some platforms (or data brokers they work with) collect, analyze, and sell consumer profiles. Although not all companies in the payments sector sell user info, the broader data broker industry can still obtain and repackage financial behavior and transaction data. This can be used for anything from targeted ads to more invasive profiling techniques.

Risk of Linking Offline and Online Identities

Even older, paper-based options like USPS Money Orders can be compromised by camera surveillance at the post office, or by a requirement to show an ID for higher amounts. Once names, addresses, or signatures are recorded, state or private investigators may combine that with digital data to build a fuller profile—especially if the mutual aid group is already flagged.

Evaluating the Tools: Cryptocurrencies and Beyond

When financial privacy is a necessity rather than a preference, choosing the right tools becomes critical. While cryptocurrencies often dominate the conversation, they aren’t the only—or always the best—option. Each method of transacting privately comes with trade-offs: some offer stronger anonymity but face regulatory hurdles, while others provide ease of use at the cost of traceability.

While the report goes into great detail with each option, below is a breakdown of the various financial privacy tools discussed. This includes privacy-focused cryptocurrencies to old-school cash alternatives, along with the advantages and challenges they present.

Bitcoin

Pros: Pseudonymous; decentralized.

Cons: The public ledger means transactions are often more traceable than people expect. Law enforcement has become quite adept at blockchain analysis, making Bitcoin less ideal for high-risk mutual aid transactions.

Monero

Pros: Strong privacy features like ring signatures and stealth addresses. This makes tracing transactions much harder.

Cons: Heavier regulatory scrutiny; trickier for the uninitiated. Also harder to convert into traditional currency because some exchanges avoid it.

MobileCoin

Pros: Specifically engineered for private, fast, mobile transactions (notably integrated into encrypted messaging apps like Signal).

Cons: Limited exchange support and relatively new, so it hasn’t been tested as widely as more established coins.

Zcash

Pros: Offers optional private (shielded) transactions using zero knowledge technology, meaning amounts, sender, and recipient can stay hidden.

Cons: Many users default to transparent transactions, negating the privacy advantage.

Non-Crypto Methods

USPS Money Orders: Essentially the old reliable. One of the most private ways to send money without a significant data trail, although you’ll need to buy them in person and keep an eye on fees.

Apple Tap-to-Cash: High-tech, in-person transactions built into the Apple ecosystem. While it can add layers of biometric security, once you top up your account you may still need to verify your identity.

CashApp: Quick and familiar, but limited anonymity. Accounts can be frozen or suspended, and transaction records are retained.

Prepaid Gift Cards: Offer a straightforward, low-tech anonymity; but they can be easily lost or stolen, and many have fees.

Privacy.com Cards: Excellent for limiting what details you share with merchants. Still, you must provide personal information to Privacy.com, and they can disable certain transaction types or categories.

Balancing Practicality and Security

There’s no one-size-fits-all solution for financial privacy. The right option depends on each individual or group’s needs and technological comfort. A small, under-the-radar queer health fund in Montclair might choose USPS money orders for near-complete anonymity, while a longstanding Brooklyn abortion fund with a tech-savvy crew might set up a pipeline with Monero or Zcash—especially if participants trust those coins’ privacy features.

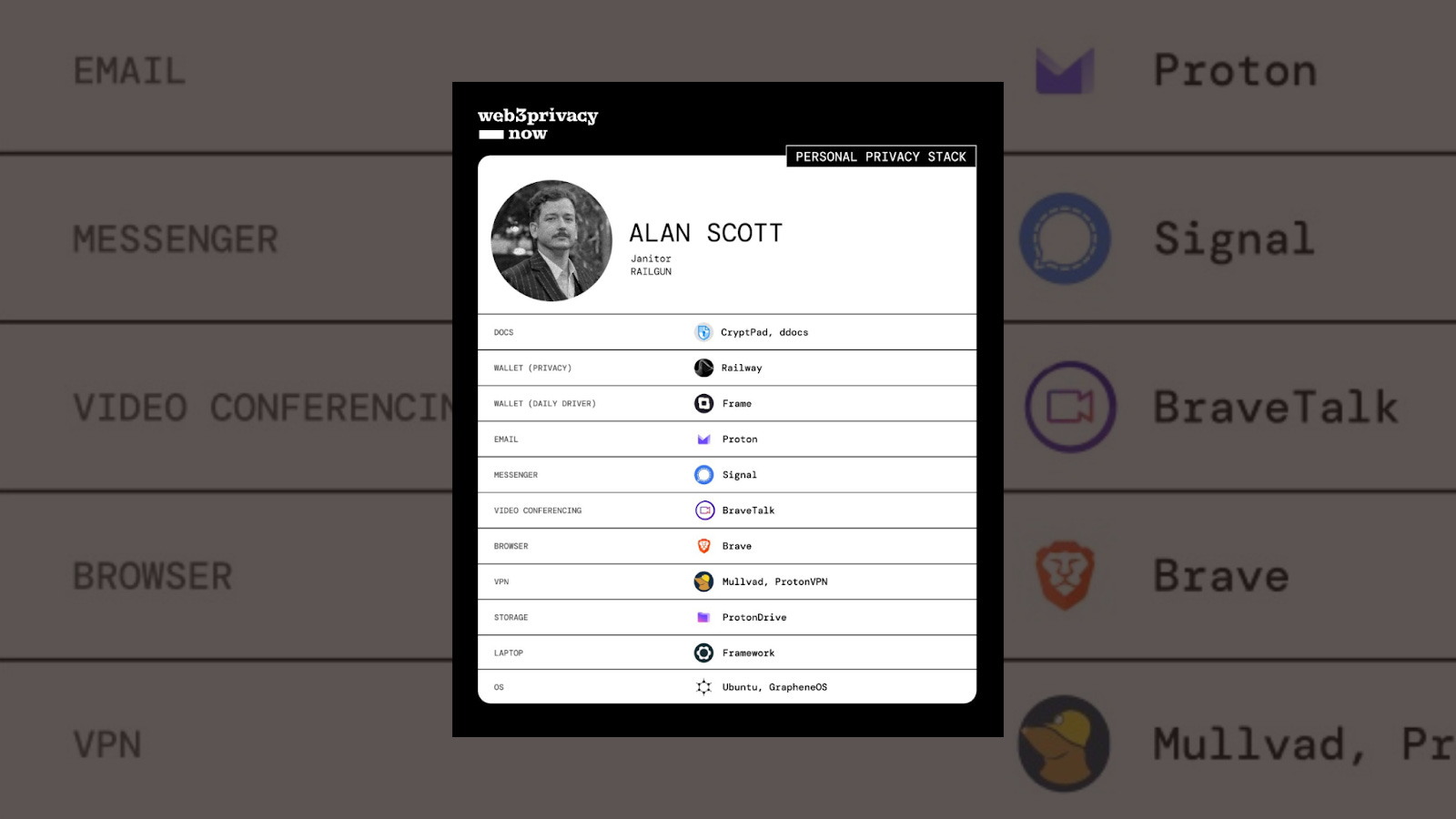

Example Personal Privacy Stack

Privacy-focused advocacy group Web3 Privacy Now shared an example personal privacy tech stack on social media that balances everyday convenience with robust security. It combines well-known open-source tools, privacy-oriented services, and hardware/software choices designed to minimize digital footprints:

Privacy-Focused Wallet: Railway

Daily-Use Wallet: Frame

Email: Proton

Messenger: Signal

Video Conferencing: BraveTalk

Browser: Brave

Cloud Storage: ProtonDrive

Laptop: Framework

Operating System: Ubuntu, GrapheneOS

A Snapshot Conclusion

The essence of mutual aid is to help each other without strings attached, whether it’s an activist art collective on the Lower East Side, a warehouse-turned-community center in Williamsburg, or a makeshift gig for Wildfire Relief in Jersey City. Yet in the digital age, few activities are left unseen. The best options, as spelled out in “Financial Confidentiality in the Age of Digital Surveillance,” combine strong privacy features with ease of use—so that good intentions aren’t stifled by tech obstacles or legal hazards.

Ultimately, each group or individual has to assess their own threat model. Are you worried about law enforcement infiltration? Personal doxing? The next wave of digital corporate surveillance? Forging safer spaces often means embracing creative, sometimes hidden, ways of operating. In today’s financial landscape, that might mean exploring a private cryptocurrency, skipping credit cards in favor of money orders, or using advanced payment apps built on modern encryption.

For the thousands of mutual aid groups channeling that old-school, underground ethos, the moral of the story is simple: We all need to keep watch for who’s watching us. Financial freedom, much like the sweaty freedom of a packed DIY show, matters for the health and safety of communities—especially those facing serious repression. And when you’re passing around the hat (physical or digital), the ability to do so privately may be more crucial than ever.

Subscribe below so you don’t miss Part II for our interview with Alan, Janitor at RAILGUN with an impeccable taste in music.